All About Required Minimum Distributions (RMDs)

by Kevin Rigg, Director of Financial Life Planning, Lead Advisor, CFP®, CPA

We have written in the past on the basics of RMDs and how SoundView helps you manage this annual requirement from the IRS (see Kevin Slater’s March 2021 article here). Today we want to explore RMD rules in a bit more detail and review some of the important rule changes put into place over the past several years.

What Are Required Minimum Distributions?

RMDs are amounts that the federal government requires you to withdraw annually from traditional IRAs and employer-sponsored retirement plans after you reach age 73 (was 72 from 2020-2022 and 70 ½ prior to 2020). The purpose of RMD rules are to ensure that people don't accumulate funds in retirement accounts indefinitely, deferring taxation and eventually leaving them as an inheritance.

Which Accounts Are Subject to the RMD Rules?

Traditional IRAs, simplified employee pension (SEP) IRAs and SIMPLE IRAs are subject to the RMD rules (Roth IRAs are not subject to these rules while you are alive). Employer-sponsored retirement plans subject to the RMD rules include qualified pension, stock bonus, and profit-sharing plans (including 401(k) plans). Section 457(b) and 403(b) plans are also subject to RMDs.

When Must RMDs Be Taken?

Your first required distribution from an IRA or retirement plan is the year in which you reach age 73 and must be taken by December 31st of that year. There are two exceptions to this general rule:

For your first distribution, you have the option to take it during the year you reach age 73, or delay taking it until April 1st of the following year. Delaying will result in taking two distributions in one year (the first by April 1st and the second by December 31st).

If you continue working past age 73 and participate in your employer's retirement plan, your first distribution is not required until April 1 following the calendar year in which you retire (if the retirement plan allows this and you own 5% or less of the company).

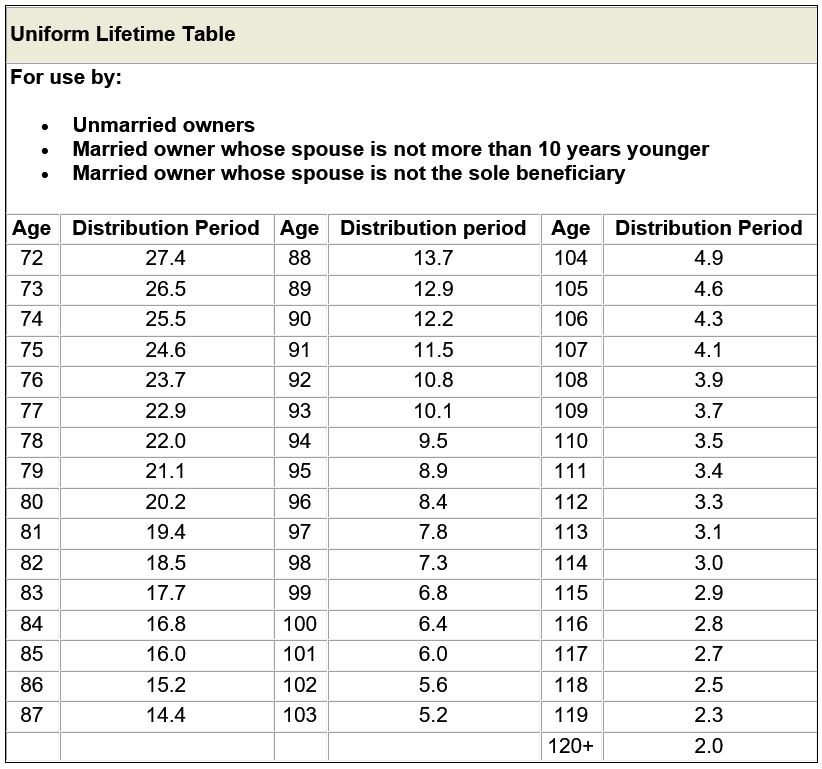

How Are RMDs Calculated?

RMDs are generally calculated by dividing your traditional IRA or retirement plan account balance on the prior December 31st by a life expectancy factor specified in IRS tables. Most taxpayers use the Uniform Lifetime Table (link here), which assumes that the account owner has designated a beneficiary who is exactly 10 years younger. If your spouse is your designated beneficiary and more than 10 years younger, you can take your RMDs over a longer payout period than under the Uniform Lifetime Table.

{kind=link}

If you have multiple IRAs, an RMD is calculated separately for each IRA. However, you can withdraw the required amount from any one or more IRAs. If you participate in more than one employer retirement plan, your RMD is calculated separately for each plan and must be paid from that plan.

What If You Fail to Take RMDs As Required?

You can always withdraw more than you are required to from your IRAs and retirement plans. However, if you fail to take at least the RMD for any year (or if you take it too late), you will be subject to a 25% excise tax on the amount by which the RMD exceeds the distributions made. If you self-correct the error within a two-year period by withdrawing the required funds and filing a return reflecting the tax, you can qualify for a lower 10% penalty rate.

RMD Tax Considerations

RMDs are generally subject to federal (and possibly state) income tax for the year in which you receive the distribution, with the following exceptions:

If you have ever made after-tax contributions to the retirement account (in which case a prorated portion of each distribution would be non-taxable).

If it is a qualified distribution from a Roth 401(k), 403(b), or 457(b) account (it is qualified if it satisfies a five-year holding period requirement).

Taxable income from an IRA or retirement plan is taxed at ordinary income tax rates even if the funds represent long-term capital gain or qualifying dividends from the investments held within the account.

Inherited IRAs and Retirement Plans

Your RMDs from your IRA or plan will cease after your death, but your non-spouse designated beneficiary (or beneficiaries) will typically be required to liquidate the account within 10 years. A spouse beneficiary may generally roll over an inherited IRA or plan account into an IRA in the spouse's own name, allowing the spouse to delay taking RMDs until turning 73.

These are only some of the important details we keep in mind when managing your RMDs each year. You can expect more conversations about any upcoming RMDs at the next meeting with your planning team, but please let them know if there is anything you would like to discuss in the meantime.